The Vice President Dr Mahamudu Bawumia is right in the sense that individualized credit-scoring does not exist in Ghana, an economist, Dr. Theo Acheampong has said.

Dr Theo Acheampong stated that although he is not an IT expert, leveraging the Ghana Card to become the anchor of the credit system and, thereby, meet the ultimate goal of a personalized credit score is a sensible idea that must be supported by all.

Dr. Bawumia announced at the 57th congregation of the Kwame Nkrumah University of Science and Technology that Ghana will introduce a credit scoring system next year to allow Ghanaians access to personal loans and also help financial institutions control the allocation of risks and costs with their clients.

It was his view that the credit system would ensure discipline in the payment of loans.

“Ghana early next year will be introducing a credit scoring system for individuals. Every individual will have a credit score. Right now, our credit scoring system does not exist.

“So, everybody is seen as risky and the interest rates are high. But we are going to go into individualized credit scores. So, if you don’t pay your loan, you will have no credit score and you will have a problem when you go for a loan. But if you are diligent in paying your loans you get your high credit score and you are likely to get lower interest rates. This will bring more discipline,” he said.

Dr Bawumia’s policy proposal received flak from some analysts including a professor at the University of Ghana Kobby Mensah who cast doubt on the ability to roll out such a policy.

In a post shared on X on November 28, 2023, Prof Mensah asked why the Ghana Card is not being used to acquire vehicles because there are garages in Ghana already.

“Are we not in Ghana? Are there no garages in Ghana? If the answers to these questions are yes, then the case is simple.

“Take your Ghana card to CFAO to pick up a Mercedes and let’s prove the theory,” he wrote

But in a write-up on his X platform, Dr Theo Acheampong said that “We must commend such policies. The policy debates have already started ahead of the 2024 elections, and some of us are here to interrogate them in detail and offer alternative pathways. It is our civic duty!”

Below is the full write-up…

DR BAWUMIAH IS RIGHT: A PERSONAL CREDIT-SCORING SYSTEM DOES NOT EXIST, AND IT IS A MUST TO DEEPEN FINANCIAL ACCESS

Vice President Dr Mahamadu Bawumiah of the ruling NPP administration recently remarked, “Ghana will introduce a credit scoring system next year for citizens [individuals], which will help citizens access personal loans and help financial institutions control the allocation of risks and costs”.

He further indicated that “right now our CREDIT-SCORING SYSTEM DOES NOT EXIST so everybody is seen as risky and the interest rates are high….But we are going to move into INDIVIDUALISED CREDIT SCORING…and that the Ghana Card will become the anchor for the credit system”.

According to the Bank of Ghana’s 2022 Credit Reporting Activity Report, there are currently three (3) licenced credit bureaus: XDS Data Ghana Limited, HudsonPrice Data Solutions Limited and Dun and Bradstreet Credit Bureau Limited. These companies operate under the Credit Reporting Act, 2007 (Act 726) and are involved in collecting credit data and providing credit referencing services to financial institutions. Furthermore, a total number of twenty-two (22) institutions and companies designated as data providers and authorized users of the credit reporting system were at various stages of full compliance (pp.8-9).

Pages 9 of the same report published by the Bank of Ghana notes that “Banks generally complied with data submission requirements and actively used the services of credit bureaus”.

Furthermore, 9.1 million searches were conducted by authorised users on individual borrowers or potential individual borrowers in 2022. Another 277,315 searches were conducted on businesses or corporate borrowers. By far, most of the searches were on individual borrowers (97%) compared with 3% of businesses.

However, it is important to note that the products and services offered by the Credit Bureaus are not INDIVIDUALISED CREDIT SCORING. Rather, these come in six (forms), namely:

“Consumer Basic Trace Report: This contains information on personal details, credit account summary, address history, guarantor details and telephone history. This is designed to help the lender in completing “know your customer” (KYC) documentation on the customer.

Consumer Basic Credit Report: This contains personal information, credit account summary, detailed credit facility status, and monthly payment behaviour.

Basic Commercial Report: It contains company registration details, directors and credit account summary. It is designed to provide background information on companies and basic information on credit exposure.

Consumer Credit Report – This contains the credit profile overview, credit profile summary, credit facility details, and demographic information. This report provides information on the credit exposure and repayment history of borrowers and empowers lenders to make better credit risk decisions.

Commercial Credit Report – This presents the credit history, demographic information and company profiles, and

Industry Reports – These include a variety of products to enhance the Know-Your-Customer (KYC) procedures of financial institutions with respect to banks’ business customers.”

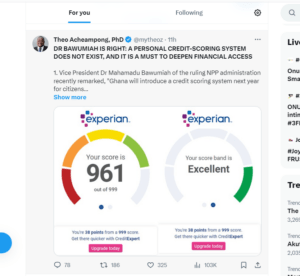

In other words, the current data provided by the credit bureaus are amalgamated reports comprising different data points such as personal details, credit account summary, address history, guarantor details and telephone history. The companies, for one reason or another, are unable to combine this information into a COMPOSITE CREDIT SCORE such as offered by the likes of companies like Experian and TransUnion here in the UK where I am based, and which can allow the pricing of individual financial products and services. In terms of evidence, I have attached my Experian score, which currently sits at 961 out of 999 and is rated excellent. With this single number, I can access various products, including credit cards, loans, insurance, and other financial products.

Dr Bawumiah is right in the sense that an INDIVIDUALISED CREDIT SCORING does not exist in Ghana.

I am by no means an IT expert, but leveraging the Ghana Card to become the anchor of the credit system and, thereby, meet the ultimate goal of a personalised credit score is a sensible idea that all must support.

We must commend such policies. The policy debates have already started ahead of the 2024 elections, and some of us are here to interrogate them in detail and offer alternative pathways. It is our civic duty!

LET’S ALL ELEVATE THE DEBATE!